Friday, June 16, 2017

Influenster VoxBox

Monday, February 13, 2017

Transferwise Review : Personal Experience (+ Free Valentine's Day Gift Included)

When I left the UK , I still had a bank account balance with my earnings from my day job. At the time I left ,in September 2015, the exchange rate was 1 GBP = 1.5162 USD. I figured I would still leave the money in the account for future transactions. I could shop online, spend during visits to the UK and I was even able to make a few transactions in the US, as expected, with the exception of a few smaller stores.

Fast forward to December 2016, Brexit happened and the reality of visiting UK had significantly diminished. I didn't have any family in the UK or business interests and I wasn't quite shopping with UK retailers. So why did I need some of my money in pounds ? Besides forex trading and currency risk hedging, I had run out of reasons. I decided to transfer my funds to my US account. The first thing I did was an international transfer through Barclays. The average market rate was 1.2366 USD/GBP on the 21st of Decemeber but I was charged 1.19 USD/GBP plus an additional fee of £15. Fortunately, for me this transaction didn't go through but I didn't realize until 3 days later.

I decided to look for other options. I checked out Paypal since I already had one but their offered price was even worse than my bank, 1.18 GBP/USD and additional transaction fees of about 3.9%. Bust! This is when I came across Transferwise! They offered live forex rates as seen on google.com, xe.com. yahoo.com and dailyfx.com etc for as low as £2. It turns out this can be up to 10 times cheaper than with the bank because it's a peer-to-peer platform. I decided to try it out! As I was using this for the first time , I assumed there was risk involved and so I opted to start with a small amount. I made the deposit on the 24th of December through my UK bank . Payment are made through your bank so you won't be sharing your password and it's safe. The average exchange rate on that day was 1.2271 USD/GBP but I was offered 1.2292 USD/GBP by TransferWise and 2 business days for processing. The exchange rate fluctuates instantaneously as with the live market rates.

In 8 minutes, I received an email that they had received my deposit.

On the 27th of December I received an email explaining the transfer was complete and to be expected the next day.

Sure enough I received my money on the 28th of December. I felt like I could safely trust Transferwise now so I transferred the rest of my funds. Unfortunately the exchange rate had weakened a little by that time, so I was a bit bumped by that ,but on the bright side it was still a lot better than the rate my bank offered me and I was given a shorter processing time of ONE business day! So I was pleased about that!

Now I am not sure why they have different processing times but they tell you before you commit to payment, so that is pretty fair. Overall, I have no complaints or negative experience. I'm happy I chose to use TransferWise vs whatever is out there. Lucky for you, the exchange rate has gone up to 1.2523 GBP/USD (14 Feb 2017) and you can get a FREE transfer here!

Happy Valentine's Day

Sunday, July 19, 2015

Scoring Systems Development

The first stage towards developing a scoring system is project preparation. In this step, the goal of the scoring system is defined, this may include an objective to improve credit decisions or to reduce the cost of decision making. Further areas to consider in the project preparation stage are the feasibility study and player identification and responsibilities. The next stage in the development of scoring system involves the preparation of data. Examples of such data prepared are demographics (e.g., age, time at residence, time at job, postal code), existing relationship (e.g., time at bank, number of products, payment performance, previous claims), credit bureau (e.g., inquiries, trades, delinquency, public records), real estate data, and so forth. Data preparation consist of six main activities namely; data acquisition, data pre-processing to treat outliers and missing values, setting the good/bad definition to derive the target variable used in the model, determining the observation and outcome windows to ensure an optimal period is chosen, selecting and formatting the independent variables and sampling design to avoid structural biases.

Once this is completed,the next step of modelling the scorecard can be started. A large by number of algorithms are available to build a scoring model; these include discriminant analysis, linear regression, logistic regression , survival analysis, neural networks and regression trees. Categorical data analysed through statistical techniques such as logistic regression have increasingly been used in PD modelling. Logistic regression models are linear models, that yields prediction probabilities for whether or not a particular outcome (default) will occur. Once a good logistic regression model has been finalized, the decision has to be made where to put the cutoff values for extending or denying credit. Correspondingly, LGD modelling is defined by a set of estimated cash flows resulting from the workout and/or collections process, properly discounted to a date of default. EAD can be modelled as a linear function of the current loan amount outstanding, the estimated time to default, the contractual rate of interest and charges incurred prior to default. The derived final model may be implemented through parameterized decision engines, such as Experian's Strategy Manager and FICO's Blaze , as well as into the application processing and decision-making systems. These allow credit professionals to directly input credit scoring models into their organization's IT system.

Finally, the evaluation process is used to confirm accuracy and monitor the performance of the model. As reject bias is inherent in classification models, a reference inference process can be utilized to estimate the behavior of previously rejected applicants.This can be further used to develop a percentage correctly classified (PCC) measure. In addition, area under the curve measures are widely used to measure the overall discrimination of the model between the distribution of good and bad cases. The most popular of these are the GINI coefficient , calculated using the Brown formula. Another widely used measure is the K-S statistics which represents the maximum difference between the cumulative proportion of each class across the range of model scores. These are particularly useful for gauging the power of a scoring model when the model will be used for setting multiple cut-off scores and evaluating scorecards when the use of the model is uncertain.

Finally, the evaluation process is used to confirm accuracy and monitor the performance of the model. As reject bias is inherent in classification models, a reference inference process can be utilized to estimate the behavior of previously rejected applicants.This can be further used to develop a percentage correctly classified (PCC) measure. In addition, area under the curve measures are widely used to measure the overall discrimination of the model between the distribution of good and bad cases. The most popular of these are the GINI coefficient , calculated using the Brown formula. Another widely used measure is the K-S statistics which represents the maximum difference between the cumulative proportion of each class across the range of model scores. These are particularly useful for gauging the power of a scoring model when the model will be used for setting multiple cut-off scores and evaluating scorecards when the use of the model is uncertain.

The accuracy of the models such as LGD and EAD are problematic to validate due to the low numbers of defaults and problems obtaining data on the amount and timing of post-default cash flows. Additionally, applicant profiles and systems change and evolve over time, and certain data items that were available for model construction may no longer be available within the operational system. Finally, the asymmetric distribution and the sensitivity to economic conditions makes its difficult to model scoring models that perform optimally over time.

Saturday, July 18, 2015

Consumer Credit Referencing and Information Sharing

A credit reference agency is an external organization which enables financial institutions and public authorities to share and retrieve information about individuals or other entities credit commitments to reach responsible decisions on credit requests. The major global credit reference agencies include Experian, Equifax and Transunion. They ensure that the right customers get affordable credit they deserve while simultaneously maintaining lower interest rates and unlawful lending. Furthermore, they may help consumers review and understand their personal credit histories and provide advice on how to improve their credit ratings.

In order to create the information provided by CRA, data is pooled from private and public sources such as application forms, past dealings, electoral roll, socio-economic surveys, financial statement and court orders. The relevant data is then integrated and cleaned into attributes and variables that implies characteristic quality which are subsequently, used to develop scoring models for predicting probabilities of default and also other phenomenons such as behavioural propensities, profitability, probability of recovery and fraud based on historical experiences. The scoring models employ parametric or machine learning technics such as : discriminant analysis, logistic regression , neural networks and genetic algorithms which are then tested and modified to ensure accuracy and predictability of the estimated credit scores. The scorecard and further reference information is retrieved from CRAs systems through a provided unique identification number.

In order to create the information provided by CRA, data is pooled from private and public sources such as application forms, past dealings, electoral roll, socio-economic surveys, financial statement and court orders. The relevant data is then integrated and cleaned into attributes and variables that implies characteristic quality which are subsequently, used to develop scoring models for predicting probabilities of default and also other phenomenons such as behavioural propensities, profitability, probability of recovery and fraud based on historical experiences. The scoring models employ parametric or machine learning technics such as : discriminant analysis, logistic regression , neural networks and genetic algorithms which are then tested and modified to ensure accuracy and predictability of the estimated credit scores. The scorecard and further reference information is retrieved from CRAs systems through a provided unique identification number. The operation of credit reference agencies is subject to privacy concerns and legislation. CRA regulations dictates compliance hierarchy of statutes, due diligence requirements, business ethics suppressing predatory and irresponsible lending and ensures that discriminatory information such as race and religion are prohibited from the information gathering process. Such regulations often vary from country to country and include the Equal Credit Opportunity Act of 1974 and the Data Protection Act of 1984.

The operation of credit reference agencies is subject to privacy concerns and legislation. CRA regulations dictates compliance hierarchy of statutes, due diligence requirements, business ethics suppressing predatory and irresponsible lending and ensures that discriminatory information such as race and religion are prohibited from the information gathering process. Such regulations often vary from country to country and include the Equal Credit Opportunity Act of 1974 and the Data Protection Act of 1984.

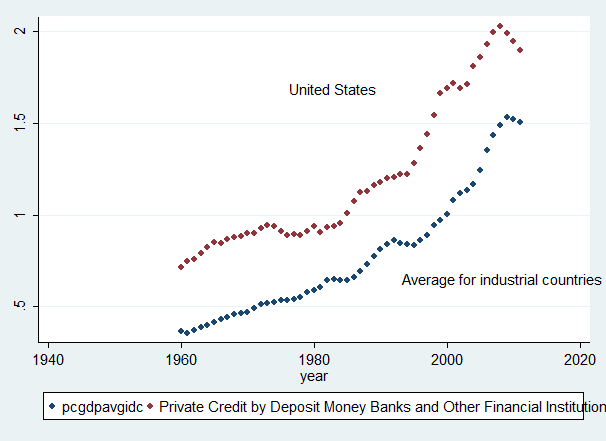

The main objective of credit scoring is to minimize the cost and improve the efficiency of the customer-facility selection process, this is particularly dependent on the degree of information sharing between the existing CRAs and financial institutions. The availability of data sharing of credit information has heighten process automation and industrialisation within the realms of credit decision-making, and thus has effectively reduced the amount of information required directly from customers, improved security and fraud tracing, reduced adverse selection and bad debt for suppliers, improved mobility, pricing and choices of credit consumers. Research indicates a strong relationship between the depth and existence of data sharing and the ratio of private credit extension to GDP. Furthermore, efficient information sharing has been linked to a reduction in transaction cost of SMEs.

However, credit data sharing faces a number of limitations. Firstly, disclosing information and computational processes encourages fellow lenders to poach and gives potential customers the tools to polish up their scores, this triggers new types of default risk and thus necessitates more frequent rebuilding and recalibrating. Secondly, the shared information may be modelled with little considerations of database biases such as the missing values, outliers, compliance constraints and the recency and representativeness of the data. Finally, information has a limited lifetime due to changing economic conditions such as the recession in the 1980s and new strategic actions undertaken by financial institutions, this ensures that data sharing remains capital intensive and complex over time.

Friday, July 17, 2015

Enhancing Business Valuation with Trade Credit

Trade credit involves supplying goods and services to business customers on a deferred payment basis (Wilson,2008) and provides access to capital for firms that are unable to raise it through more traditional channels. The shift from the isolated, traditional practice of credit management toward the more technologically advanced and integrated credit management of today has enabled firms to efficiently maximize investment in profitable-customers and minimize risk. The fast-changing credit management practices has played an important role towards reforming the credit policies, customer relationship management, credit services and marketing tools employed by organization, globally.

Extending trade credit is used as a vital extension of short-term financing and as a strategic tool to improve administrative efficiencies, build trust and enhance business development. However, converting debtors into cash in a cost effective, efficient, dispute free and timely manner is crucial to the financial health of any business. Therefore, organization must engage an effective collection strategy to minimize bad debt, financing costs and collection cost. This involves assessing and understanding customer potential income and their risk , tailoring credit terms to reflect the risk through out the economic cycle, and on converting trade debts into cash flow with certainty while bearing practical cost constraints. In a number of ways, this process helps in boosting current profitability, expected earnings growth and liquidity which are ultimately imperial to driving shareholder value.

The granting of credit can signal to customers that the business has confidence in the quality of goods supplied and wants to establish a long-term relationship. This is beneficial to the firm issuing trade credit as it helps in generating repeat purchase behaviour, signals financial strength and establishes reputation in the mist of competition(Finlay,2010).Additionally, trade credit may allow suppliers to price discriminate using credit when discrimination directly through prices is not legally permissible. For example, a firm may informally revise late payments from some customers without penalty or grant discounts outside of the discount period for favoured customers. There is much scope for flexibility and for treating clients distinctively relying upon their importance, short-term financial circumstances, the opportunity for creating repeat businesses or, of course, the relative bargaining position (Wilson,2014).

Furthermore, trade credit, in itself is, useful in reducing transaction costs and collecting valuable information about customers (Petersen,1997). For example, businesses can reduce fixed cost from the number of invoices, shipment and cash handling and increase sales volume by introducing minimum order quantity restrictions with formal credit terms. Analysing the credit choices of buyers and the operations of their customers through their normal course of business , organizations are able to gather information about when the customers need to be monitored more closely, whether credit terms must be modified, or whether the supply of products should be halted for a particular risky customer (Cuñat, 2012).

Finally, credit management can be out-sourced to specialised institutions that perform the various credit administration functions. These include factoring services to a form of advance against a company’s trade receivables and collect outstanding balances on behalf of the company, credit insurance to provide effective means of alleviating late payment problems for example trade credit insurers provided SME's with cover worth up to £25.7 million for goods supplied to Phones 4u whe it was put into administration in 2014, improving credit management discipline and protecting against protracted default or bad debt and credit reference agencies to provide information on potential customers to aid organizations in deciding who is creditworthy and who is not based on credit scoring and judgmental decision rule.

Extending trade credit is used as a vital extension of short-term financing and as a strategic tool to improve administrative efficiencies, build trust and enhance business development. However, converting debtors into cash in a cost effective, efficient, dispute free and timely manner is crucial to the financial health of any business. Therefore, organization must engage an effective collection strategy to minimize bad debt, financing costs and collection cost. This involves assessing and understanding customer potential income and their risk , tailoring credit terms to reflect the risk through out the economic cycle, and on converting trade debts into cash flow with certainty while bearing practical cost constraints. In a number of ways, this process helps in boosting current profitability, expected earnings growth and liquidity which are ultimately imperial to driving shareholder value.

The granting of credit can signal to customers that the business has confidence in the quality of goods supplied and wants to establish a long-term relationship. This is beneficial to the firm issuing trade credit as it helps in generating repeat purchase behaviour, signals financial strength and establishes reputation in the mist of competition(Finlay,2010).Additionally, trade credit may allow suppliers to price discriminate using credit when discrimination directly through prices is not legally permissible. For example, a firm may informally revise late payments from some customers without penalty or grant discounts outside of the discount period for favoured customers. There is much scope for flexibility and for treating clients distinctively relying upon their importance, short-term financial circumstances, the opportunity for creating repeat businesses or, of course, the relative bargaining position (Wilson,2014).

Furthermore, trade credit, in itself is, useful in reducing transaction costs and collecting valuable information about customers (Petersen,1997). For example, businesses can reduce fixed cost from the number of invoices, shipment and cash handling and increase sales volume by introducing minimum order quantity restrictions with formal credit terms. Analysing the credit choices of buyers and the operations of their customers through their normal course of business , organizations are able to gather information about when the customers need to be monitored more closely, whether credit terms must be modified, or whether the supply of products should be halted for a particular risky customer (Cuñat, 2012).

Finally, credit management can be out-sourced to specialised institutions that perform the various credit administration functions. These include factoring services to a form of advance against a company’s trade receivables and collect outstanding balances on behalf of the company, credit insurance to provide effective means of alleviating late payment problems for example trade credit insurers provided SME's with cover worth up to £25.7 million for goods supplied to Phones 4u whe it was put into administration in 2014, improving credit management discipline and protecting against protracted default or bad debt and credit reference agencies to provide information on potential customers to aid organizations in deciding who is creditworthy and who is not based on credit scoring and judgmental decision rule.

Thursday, July 2, 2015

The Scale of Gender Polarity

Culture and its social norms determines the set of traits, behaviours, and roles that defines masculinity and femininity. Both of which are to be opposite of one another, but at the same time complement each other. You can't take gender and try to redefine it to suit your idealistic principles. It's already been defined by the Association of Societal and Cultural Maintenance (ASCM) and can be visually represented on the scale of gender polarity.

On this scale, we assign masculine the value of +1 , neuter the value of 0 and feminine the value of -1 . Gender polarity exists in order to motivate the two sexes (male and female) to desire one another and to find fullness in their union. The gender polarity does not represent anomalies such as those where one is born an intersex or a gender that does not align with their assigned sex at birth.

Some of these specified attributes include facial features that can be represented visually on a similar polarity scale, as femininity draws closer to masculinity, the eyebrows become bushier, the lips become thinner, the eyes become narrower, the nose widens, the jawline become more defined, etc. This defines what is beautiful in a woman and handsome in a man. Note that ugliness does not exist on this scale. The state of being unattractive is of no benefit to society and as such is an undesirable attribute to either sexes.

Some of these specified attributes include facial features that can be represented visually on a similar polarity scale, as femininity draws closer to masculinity, the eyebrows become bushier, the lips become thinner, the eyes become narrower, the nose widens, the jawline become more defined, etc. This defines what is beautiful in a woman and handsome in a man. Note that ugliness does not exist on this scale. The state of being unattractive is of no benefit to society and as such is an undesirable attribute to either sexes.

Other's include more intangible attributes. Obviously both gender characteristics can consist of positive and negative attributes . For example a positive feminine attribute can be kindness while a negative feminine attribute may be incompetence. A basic summary of these attributes can be represented below.

{kind=link}

Naturally some cisgender females and males would find that they tend to exhibit traits that are attributed to the opposite gender. Not to worry, this may comes up from time to time and usually depends on the situation you may find yourself in, but inevitably it would serve you better to suppress those instincts, you fight your nature and thereby inhibit your ability to attract, love and be loved by a man/woman.

Wednesday, June 3, 2015

The Failures of SEC and FASB

In the US, the legal and regulatory framework ensuring the reliability of accounting information has been around since the establishment of the AICPA and its predecessors dating back to 1887. The AICPA committee began by formally establishing accountancy in the United States as a profession through educational requirements, a code of professional ethics, licensing status and, most importantly, setting generally accepted accounting principles for financial statement accounting.

The goal of the SEC in financial accounting was to ensure improved disclosure and protect investors. However, with the collapse of Enron and WorldCom, the legal framework faced intense pressures for redevelopment. This resulted in the passage of the Sarbanes-Oxley law that established increased securities regulation and the Public Company Accounting Oversight Board (PCAOB) to maintain audit independence, enforce compliance and regulate the auditing environment. In response to Arthur Andersen shredding implicating documents, tampering was recorded as a criminal offence and auditing firms were required to maintain seven years of records relevant to their audits. Furthermore, internal controls were mandated to promote enhanced disclosures of off-balance sheet transactions

and pro-forma figures, such as with the use of SPEs and mark-to-market accounting in Enron , with senior executives taking individual responsibility for the accuracy of financial reports.

and pro-forma figures, such as with the use of SPEs and mark-to-market accounting in Enron , with senior executives taking individual responsibility for the accuracy of financial reports.

The developments in the legal and regulatory frameworks are commendable, however several limitations pose a threat to the effectiveness of the the SEC and FASB. These threats consequently transpire into large-scale accounting fraud, such as the AIG Scandal in 2005, Lehman Brothers Scandal in 2008 and Autonomy Scandal in 2012. The main limitation of the legal system stems from timeliness and adequacy of investigations, insufficient persecution and lax protection for whistleblowers. Though, the SEC budget has doubled since the SOX act was enacted the

investigation process has remained fairly constant, relying primarily on informal inquiry and witness testimonials.

investigation process has remained fairly constant, relying primarily on informal inquiry and witness testimonials.

While tips are vital towards the timely uncovering of financial statement frauds, the subpar witness protections fails in providing an incentive for compelling witnesses, particularly those not involved in the fraudulent reporting. For example, executives , Timothy Belden and Ken Rice, both involved in the accounting scheme avoided jail time and gained protection for their unethically earned fortune while neutral whistleblower, Sherron Watkins of Enron and Cynthia Cooper of WorldCom, were publicly shamed. Therefore, the SEC should seek to provide adequate compensation and/or protection to whistleblowers or divert the majority of funding towards technical forensic investigation such as data-mining, artificial intelligence and latent semantic indexing. In addition, the benefits derived from fraudulent accounting to the perpetrators, often outweighs the cost. For example, the SEC failed to prosecute Lehman Brothers citing lack of evidence and the CEO of AIG faced no criminal charges with the proceedings focused mainly on negotiating monetary fines.

The main limitation of the regulatory system stems from the flexibility within GAAP and the effects of politics in the standard-setting process. As a principle-based accounting standard, US GAAP tends to be more susceptible to aggressive reporting decisions, in comparison to rule-based accounting standard. This is evident in the choices in accounting for goodwill, recognition of special purpose entities, treatment of loans and conditions for capitalization that were extensively manipulated by Enron and WorldCom towards the interest of the executives. The interaction of private-interest groups in the accounting standard process also dilutes the true-and-fair notion that FASB frameworks claims to uphold. For example, Enron and its auditor, Arthur Andersen, were given permission to use mark-to-market accounting in 1992 after extensive lobbying efforts.

The SEC and FASB claim to be responsible for protecting investors from mishaps in the capital markets. However, numerous studies and evaluations indicate limited improvements in investor protection particularly with regards to the increase in regulation and compliance cost. The points above provide a non-exhaustive summary of the limitations of the legal and regulatory organizations in the US, further improvements include educating the public about securities markets , warning investors of fraud and stock market scams and limiting the relationship between publicly-traded companies and Wall Street.

The SEC and FASB claim to be responsible for protecting investors from mishaps in the capital markets. However, numerous studies and evaluations indicate limited improvements in investor protection particularly with regards to the increase in regulation and compliance cost. The points above provide a non-exhaustive summary of the limitations of the legal and regulatory organizations in the US, further improvements include educating the public about securities markets , warning investors of fraud and stock market scams and limiting the relationship between publicly-traded companies and Wall Street.

Subscribe to:

Posts (Atom)