A credit reference agency is an external organization which enables financial institutions and public authorities to share and retrieve information about individuals or other entities credit commitments to reach responsible decisions on credit requests. The major global credit reference agencies include Experian, Equifax and Transunion. They ensure that the right customers get affordable credit they deserve while simultaneously maintaining lower interest rates and unlawful lending. Furthermore, they may help consumers review and understand their personal credit histories and provide advice on how to improve their credit ratings.

In order to create the information provided by CRA, data is pooled from private and public sources such as application forms, past dealings, electoral roll, socio-economic surveys, financial statement and court orders. The relevant data is then integrated and cleaned into attributes and variables that implies characteristic quality which are subsequently, used to develop scoring models for predicting probabilities of default and also other phenomenons such as behavioural propensities, profitability, probability of recovery and fraud based on historical experiences. The scoring models employ parametric or machine learning technics such as : discriminant analysis, logistic regression , neural networks and genetic algorithms which are then tested and modified to ensure accuracy and predictability of the estimated credit scores. The scorecard and further reference information is retrieved from CRAs systems through a provided unique identification number.

In order to create the information provided by CRA, data is pooled from private and public sources such as application forms, past dealings, electoral roll, socio-economic surveys, financial statement and court orders. The relevant data is then integrated and cleaned into attributes and variables that implies characteristic quality which are subsequently, used to develop scoring models for predicting probabilities of default and also other phenomenons such as behavioural propensities, profitability, probability of recovery and fraud based on historical experiences. The scoring models employ parametric or machine learning technics such as : discriminant analysis, logistic regression , neural networks and genetic algorithms which are then tested and modified to ensure accuracy and predictability of the estimated credit scores. The scorecard and further reference information is retrieved from CRAs systems through a provided unique identification number. The operation of credit reference agencies is subject to privacy concerns and legislation. CRA regulations dictates compliance hierarchy of statutes, due diligence requirements, business ethics suppressing predatory and irresponsible lending and ensures that discriminatory information such as race and religion are prohibited from the information gathering process. Such regulations often vary from country to country and include the Equal Credit Opportunity Act of 1974 and the Data Protection Act of 1984.

The operation of credit reference agencies is subject to privacy concerns and legislation. CRA regulations dictates compliance hierarchy of statutes, due diligence requirements, business ethics suppressing predatory and irresponsible lending and ensures that discriminatory information such as race and religion are prohibited from the information gathering process. Such regulations often vary from country to country and include the Equal Credit Opportunity Act of 1974 and the Data Protection Act of 1984.

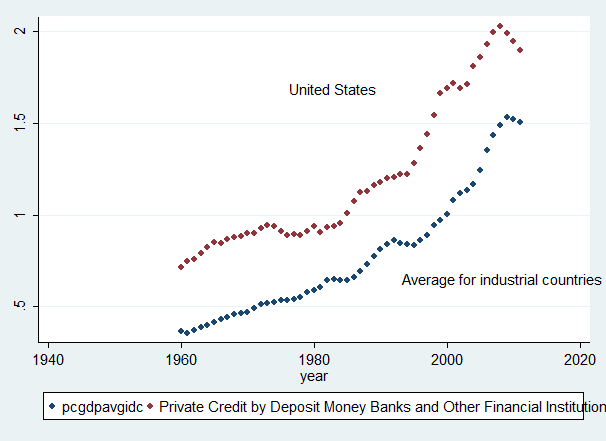

The main objective of credit scoring is to minimize the cost and improve the efficiency of the customer-facility selection process, this is particularly dependent on the degree of information sharing between the existing CRAs and financial institutions. The availability of data sharing of credit information has heighten process automation and industrialisation within the realms of credit decision-making, and thus has effectively reduced the amount of information required directly from customers, improved security and fraud tracing, reduced adverse selection and bad debt for suppliers, improved mobility, pricing and choices of credit consumers. Research indicates a strong relationship between the depth and existence of data sharing and the ratio of private credit extension to GDP. Furthermore, efficient information sharing has been linked to a reduction in transaction cost of SMEs.

However, credit data sharing faces a number of limitations. Firstly, disclosing information and computational processes encourages fellow lenders to poach and gives potential customers the tools to polish up their scores, this triggers new types of default risk and thus necessitates more frequent rebuilding and recalibrating. Secondly, the shared information may be modelled with little considerations of database biases such as the missing values, outliers, compliance constraints and the recency and representativeness of the data. Finally, information has a limited lifetime due to changing economic conditions such as the recession in the 1980s and new strategic actions undertaken by financial institutions, this ensures that data sharing remains capital intensive and complex over time.

No comments:

Post a Comment